The Untold Story Behind Ethio Telecom’s Share Sale: A Debate Every Ethiopian Investor Must Hear

In a time when inflation was running rampant, monetary policies were tightening, and global markets were bracing for recession, an unlikely hero emerged on Ethiopia’s financial scene: a defensive stock opportunity rooted in stability, resilience, and growth. While some worried about the uncertainty of dividends, savvy investors looked deeper — at the defensive nature, growth potential, and diversification benefits that made Ethio Telecom a once-in-a-decade opportunity. In this article, we'll break down: Why market value often tells a richer story than book value. How Ethio Telecom stood out as a defensive and growth stock hybrid. Why diversification — minimizing unsystematic and systematic risks — mattered more than ever. And how macro-economic conditions made Ethio Telecom the investment of choice for smart portfolios. Buckle up: the market doesn't always reward the impatient — but it always honors those who see beyond the obvious.

ECONOMY AND STOCK MARKET

By Dr. Abush Ayalew | Author and Global Financial Market Expert

4/28/20259 min read

When Ethio Telecom — Ethiopia’s flagship telecom giant — announced the launch of its historic pre-IPO share offering in October 2024, the excitement was tangible. For the first time in Ethiopia’s history, citizens were invited to own a piece of the nation’s most profitable and strategic enterprise. A company serving more than 70 million subscribers, with decades of dominance, robust profits, and a bright future in Ethiopia’s digitizing economy.

Yet, what followed defied all expectations. After a four-month offering period, ending in February 2025, Ethio Telecom only managed to sell about 10.7% of its intended shares. Out of a goal to sell 100 million shares priced at 300 Ethiopian Birr (ETB) each, just around 10.7 million shares were subscribed, raising approximately 3.2 billion ETB — far below the anticipated 30 billion ETB.

How could a seemingly perfect opportunity meet such unexpected hesitation? Superficial answers came fast: blame the economy, blame overpricing, blame lack of liquidity and dividend uncertainty. But the truth is far richer, deeper, and more revealing about Ethiopia’s financial landscape than any headline captured.

Let’s dive into the real debate.

Misunderstandings that Clouded the Opportunity

Much of the early conversation around Ethio Telecom’s undersubscription has been clouded by financial misunderstandings — misconceptions that seasoned investors worldwide would easily spot.

One of the loudest claims was that Ethio Telecom’s share price was "too high" compared to its par value or book value. But to anyone familiar with markets, this argument is fatally flawed.

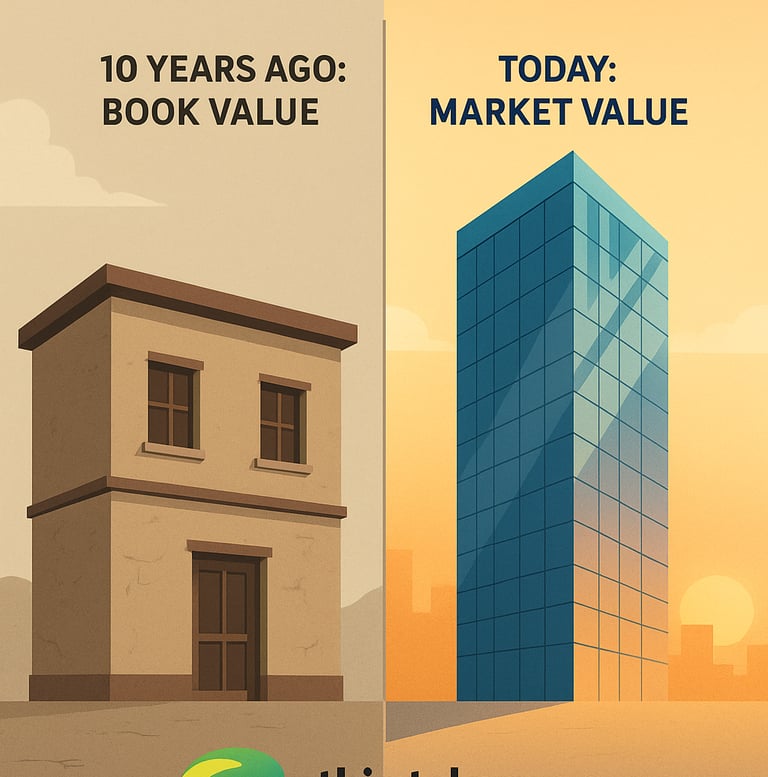

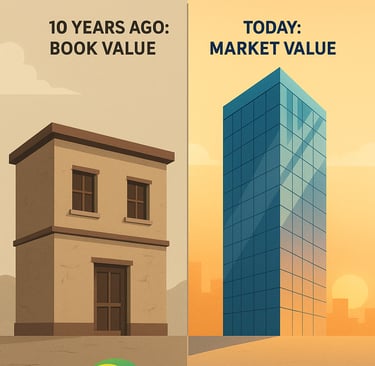

Par value — or legal minimum value — has almost no relation to real market value. To illustrate: imagine a building constructed ten years ago at a cost of 100 million Birr. Its original "book value" sits in accounting records. However, today, due to rising land values, economic growth, and strategic location, the market might price it at 1 billion Birr. Conversely, if the building were abandoned, depreciated, or located in a declining area, its market price could fall to 50 million Birr, even lower than its book value.

Assets — whether buildings or telecom companies — are valued not based on their historical cost but on future income generation, strategic importance, and market sentiment.

The price of 300 ETB per share for Ethio Telecom was informed by a careful independent valuation, led by Deloitte, based on projected cash flows, brand power, and growth potential. Compared to regional peers, Ethio Telecom was, in fact, conservatively priced.

Thus, criticism rooted in par value thinking only revealed the financial illiteracy still prevalent in the market — not a real flaw in Ethio Telecom’s offering.

The Macroeconomic Mirage: Why Tough Times Should Have Favored Telecom

Another common explanation blamed Ethiopia’s macroeconomic challenges: inflation, currency depreciation, political instability.

True, Ethiopia is weathering an economic storm. Inflation stands at around 16%, the birr continues to weaken against foreign currency baskets, unemployment pressures are growing, and the National Bank of Ethiopia has embarked on monetary tightening to combat price instability. But ironically, such economic headwinds should have made Ethio Telecom’s stock more attractive, not less.

Telecoms are classic examples of defensive stocks — companies whose services people cannot easily cut back on even during recessions. In downturns, sectors like banking, real estate, hospitality, and manufacturing suffer, while telecommunications, healthcare, food, and utilities often outperform.

Global evidence abounds. Others pointed to Ethiopia’s struggling economy, suggesting that tough times inevitably lead to poor IPO performance. Yet history tells a different story. In 2008, amidst the worst global financial crisis since the Great Depression, Kenya’s Safaricom launched its IPO — and it was oversubscribed by 532%. Telecom companies, by their very nature, provide services as essential as food, electricity, and transportation. People pay their phone bills even when they tighten every other belt. During COVID-19 lockdowns, telecom stocks globally outperformed cyclical sectors.

In Ethiopia, as real estate slows, hotels shrink, and banks tighten lending, Ethio Telecom’s revenue — from calls, internet, and mobile money services — remains vital and resilient.

For investors seeking stability during periods of domestic economic uncertainty, political instability, monetary policy tightening, and global economic recession fears amidst trade war, Ethio Telecom should have been the natural safe haven.

Thus, macroeconomic excuses do not stand.

The Myth of Overvaluation: A Reality Check

Some experts shouted about Ethio Telecom being overvalued. Again, deeper analysis reveals the opposite.

Ethio Telecom’s Price-to-Earnings (P/E) ratio, based on its last audited profits and the IPO price of 300 ETB, implied a P/E of around 15.8x — extremely low compared to Africa Telecom industry P/E average, which is around 18x. Globally, investors pay high premiums for strong, cash-generating, low-debt businesses with market monopolies — exactly Ethio Telecom’s profile.

Some self-proclaimed “analysts” have rushed to label Ethio Telecom as overvalued — yet they fail to offer any valuation models, benchmarks, or comparative data to justify their claims. Such ungrounded statements only deepen public confusion and weaken investor confidence. Critical analysis is welcome — but it must be backed by facts, not assumptions.

In U.S. markets, companies like Amazon, Tesla, and Nvidia have historically traded at 50x, 100x, even 200x earnings because investors buy into future growth, not just static earnings. The investment principle in such growth stocks is not the usual buy low and sell high approach but of buy high and sell high ones.

Moreover, Ethio Telecom combines characteristics of both a defensive stock (cash flow stability) and a growth stock (expanding into mobile money, 5G, regional markets). Growth stocks naturally attract higher valuation multiples.

Thus, the truth is Ethio Telecom was likely undervalued, not overvalued.

A Forgotten Reason: Diversification

Another powerful but overlooked argument for investing in Ethio Telecom is portfolio diversification.

For local Ethiopian investors, whose portfolios are heavily concentrated in banks, real estate, or small private businesses, buying into Ethio Telecom would have reduced unsystematic risks — risks specific to a single company or industry.

For potential foreign investors (if allowed), Ethio Telecom would have offered diversification benefits against systematic global risks, such as recession fears, tightening monetary policies, and geopolitical uncertainties.

In every modern portfolio theory, diversification is the only “free lunch” — a way to increase returns while minimizing risks. By adding Ethio Telecom’s stable, growing cash flows to a portfolio of cyclical, fragile businesses, investors would have improved their risk-return balance significantly.

Thus, beyond valuation and cash flow, Ethio Telecom’s shares offered a strategic portfolio management benefits.

What Truly Went Wrong: Deep Structural Gaps

There’s a popular whisper floating around: “Ethio Telecom’s pre-IPO failed because there’s no liquidity.” But when we take a closer look at Ethiopia’s financial history, that claim starts to unravel.

Myth of Liquidity: A Scapegoat

Consider traditional bank share sales like "Axion" — they achieved massive oversubscriptions without a stock exchange, without any liquidity events, without guaranteed dividend schedules, and certainly without proven profitability. And yet, thousands of Ethiopians eagerly lined up to invest, driven purely by trust in the founders and belief in the mission. Liquidity wasn’t the magnet — emotional trust was.

Ethio Telecom’s Liquidity Promise Failed to Excite

Ironically, Ethio Telecom offered something those early banks never dared: a real, formal promise of liquidity. For the first time in Ethiopia’s history, investors were offered a clear exit route through the newly launched Ethiopia Securities Exchange. And yet — undersubscription. Clearly, the liquidity argument doesn’t hold water. If traditional investments with far higher illiquidity risks succeeded massively, why didn’t Ethio Telecom’s?

Financial Literacy: The Hidden Barrier

The real culprits lie elsewhere. First and foremost is the massive financial literacy gap. Ethiopia is just stepping into the age of public equity investing, and for many retail investors, even for some popular professionals, basic concepts like total return are unfamiliar.

Dividend Myopia vs. Total Return Thinking

Many were misled into comparing Ethio Telecom’s projected dividend yield alone to bank savings rates and wrongly concluded that the returns were “too low.” What they missed was the giant upside of potential capital appreciation once the shares begin trading on the open market. This isn’t just an Ethiopian phenomenon — even in Nigeria, MTN had to launch a nationwide education campaign ahead of its IPO to demystify equity investing and spark massive participation. Financial literacy is not optional. It is foundational.

The Trust Deficit: Government Ownership Woes

Another force working against Ethio Telecom was the deep-seated mistrust of government ownership. Despite being profitable and operationally strong, Ethio Telecom’s status as a government-owned enterprise triggered old fears among investors: the fear of political interference, of regulatory shocks, and of bureaucratic inefficiencies eroding corporate success over time.

The Power of People: Why Founders Matter

Traditional bank share sales like Axion succeeded because investors trusted the people behind the brand — charismatic founders who embodied vision and integrity. With Ethio Telecom, there was no familiar face except the CEO, and the prime minister, only a sprawling bureaucracy. Global history warns us here too: Telkom Kenya’s IPO faced similar hurdles due to public skepticism toward government-led ventures.

Digital-Only Sales Strategy: A Misread of the Market

The sales and distribution strategy also faltered. Relying almost exclusively on Telebirr for share purchases alienated large segments of the population — older investors who prefer cash, rural populations without smartphone access, and many others uncomfortable with digital transactions. In contrast, Safaricom’s IPO in Kenya succeeded because it blended physical presence, mobile agents, banks, brokers, and digital platforms to reach every potential investor. Ethio Telecom’s digital-first strategy was ambitious, but Ethiopia’s readiness was overestimated.

Emotional Disconnect: Investing with the Heart

Beyond mechanics, there was an emotional gap. In Ethiopia’s investing culture, emotional connection matters deeply. People invest not just with their heads but with their hearts — in relationships, in founders, in dreams. Ethio Telecom, however strong its fundamentals, felt impersonal to many. No familiar founders, no family ties, no inspirational vision pitched directly to the people. And psychology teaches us: in emerging markets, emotional trust is the bedrock of financial risk-taking.

Lessons from Africa and Asia: IPOs That Won Hearts and Wallets

Across Africa and Asia, telecom IPOs succeeded by doing more than offering shares. They educated months in advance, sold aspirational narratives, created nationwide buzz, and provided multiple easy channels for purchasing shares. If Ethio Telecom had embarked on a year-long, aggressive public education campaign, set up physical sales points across cities and countryside, engaged respected community figures to build emotional trust, and blended digital with physical outreach, the story today could have mirrored the massive successes of Safaricom and MTN.

A Roadmap for the Future: Rebuilding Trust and Readiness

Looking ahead, there are critical lessons for Ethiopia’s investment future. National financial literacy drives are urgently needed — demystifying basic concepts like capital gains, total return, portfolio diversification, and risk management. Share sales must combine digital platforms like online brokerages with traditional banks, brokerage houses, and mobile agents.

Moreover, independent governance structures must be introduced to reassure minority investors, including stronger shareholder rights protections and independent board members.

Engage, Educate, Embrace: The Way Forward for Ethiopia’s Capital Market

Emotional and aspirational narratives should be woven into investment pitches — not just technical financial figures. Ethiopia’s large and wealthy diaspora must also be actively engaged. Most importantly, communication must be constant, transparent, and two-way, not just during sales windows but year-round.

Why Tax Incentives Matter: Global Lessons for Ethiopia’s Capital Market

If Ethiopia is serious about unlocking the full potential of its upcoming stock exchange and ensuring successful public offerings, tax incentives must be part of the policy toolkit. Globally, emerging markets have used such tools not only to stimulate initial investor participation but also to enhance long-term market liquidity, build confidence, and widen the investor base.

Here’s how it has worked elsewhere:

To boost IPO participation in the 2006 KenGen and 2008 Safaricom IPOs, the Kenyan government offered temporary tax reductions on dividend withholding tax and capital gains, and worked with commercial banks to provide soft loans to IPO participants.

Rwanda, one of Africa’s fastest financial reformers, introduced tax credits for first-time investors in public offerings and 0% tax on capital gains for investments held longer than 5 years.

Conclusion: Ethiopia’s Financial Dawn is Breaking

In conclusion, Ethio Telecom’s undersubscription is not a sign of failure. It’s a growing pain. A vital signpost on Ethiopia’s journey from a traditional savings culture to a vibrant investment-driven economy. For seasoned investors who see beyond the noise, one principle remains eternal: Price is what you pay; value is what you get. Ethio Telecom, with its dominant market position, solid cash flow, national and continental expansion opportunities, remains a sleeping giant. Those who understand these dynamics and act boldly today may well ride Ethiopia’s first telecom success story into the future. Because in investing — just like in life — it’s not the loudest voices that build wealth. It’s the most informed, the most courageous, and the most visionary.

The story of Ethio Telecom’s IPO is not a tragedy. It is a beginning — a first imperfect step toward building an inclusive, dynamic, and world-class capital market in Ethiopia.

In five years, ten years, we may look back and recognize this moment not as a failure, but as the necessary growing pains of a giant awakening. Ethiopia is rich with human potential, entrepreneurial spirit, and ambition. With deliberate reforms, aggressive education, and trust-building, Ethiopia can and will join the ranks of Africa’s financial leaders.

The rain of opportunity is coming again.

This time, let’s not bring a thimble.

Let’s bring the biggest bucket we can find.

The future is calling — and it’s time to answer boldly.

Disclaimer:

This article is for informational and educational purposes only and does not constitute financial advice, investment recommendations, or an endorsement of any security, company, or investment strategy. Readers are encouraged to conduct their own research and consult with licensed financial advisors before making any investment decisions. The views expressed are those of the author and are based on publicly available information and personal analysis.

About the Author

Dr. Abush Ayalew is an author and global financial market expert with deep expertise across Europe and the United States. As a graduate of Lincon University with gold medal in MBA Finance, and an MD/MBA, he brings a unique blend of medical precision, business acumen, and strategic insight to capital market development and financial education initiatives. He is the founder of Adwa Transformation Center, dedicated to democratizing financial knowledge for Ethiopia and beyond. You can rich him via abushayalew@gmail.com or Whatsup : +251911404792.